The global energy transition is no longer a peripheral ambition but a central pillar of international policy and corporate strategy. As the world races toward net-zero emissions by 2050, hydrogen has emerged as the “Swiss Army knife” of decarbonization. Among its various “colors,” Blue Hydrogen—produced from natural gas integrated with Carbon Capture and Storage (CCS)—is currently taking center stage as the most pragmatic, scalable, and cost-effective bridge between the fossil-fuel past and the green-hydrogen future.

Market Overview and Growth Trajectory

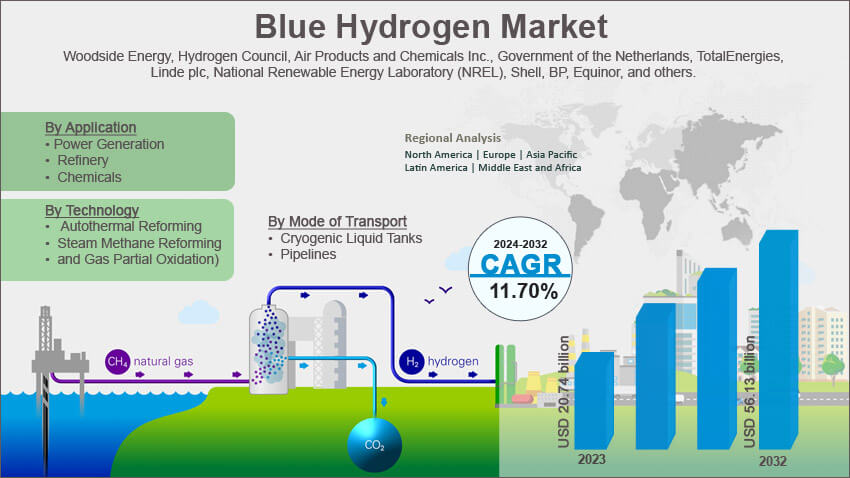

The Blue Hydrogen Market is entering a phase of exponential growth as industrial-scale projects move from final investment decisions (FID) to active construction. As of 2025, the global blue hydrogen market is valued at approximately USD 23.2 billion to USD 25 billion, according to leading industry benchmarks.

The sector is projected to maintain a robust Compound Annual Growth Rate (CAGR) of 12.5% to 14.8% over the next decade. By 2035, the market is forecast to reach a valuation between USD 86.7 billion and USD 134.4 billion. This surge is driven by the immediate need for low-carbon feedstocks in heavy industries that cannot easily be electrified, such as steel manufacturing, chemical production, and heavy-duty shipping.

| Metric | Estimated Value (2025) | Projected Value (2035) | Expected CAGR |

| Market Size | ~$24.8 Billion | ~$89.5 – $134 Billion | 13.3% – 15% |

| Leading Region | North America (42%) | North America / Asia-Pacific | N/A |

| Dominant Tech | Steam Methane Reforming | Autothermal Reforming (ATR) | 24.8% (for ATR) |

Technology Segmentation: SMR vs. ATR

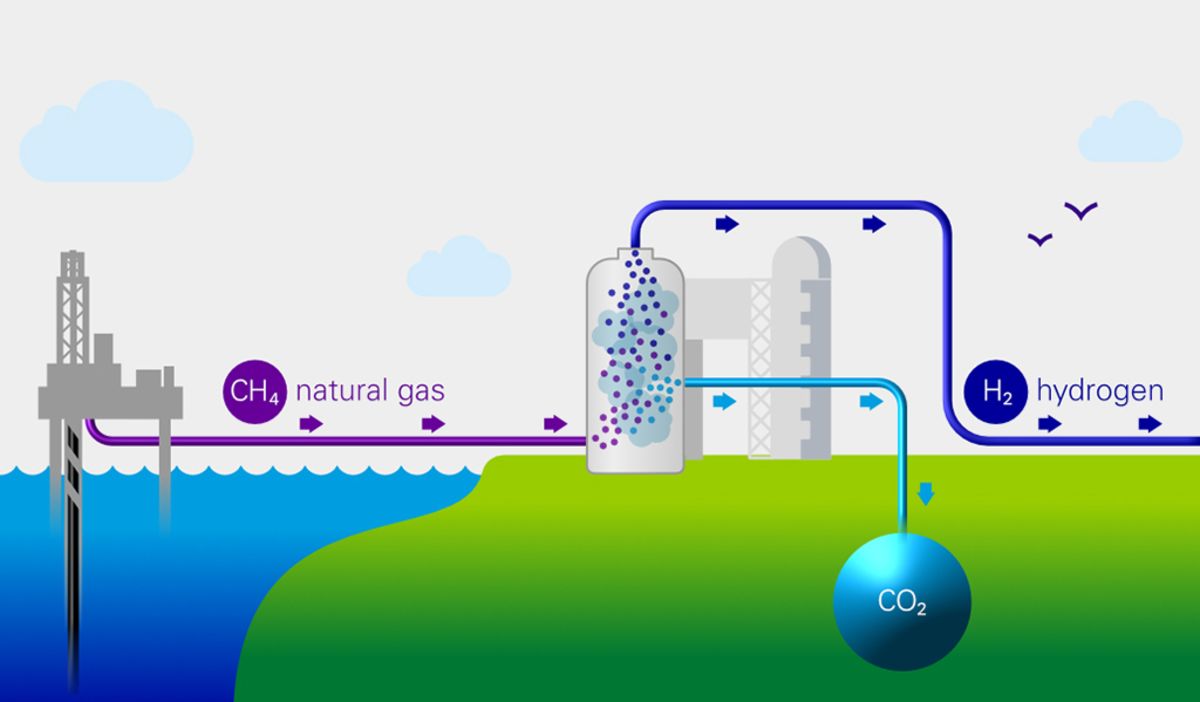

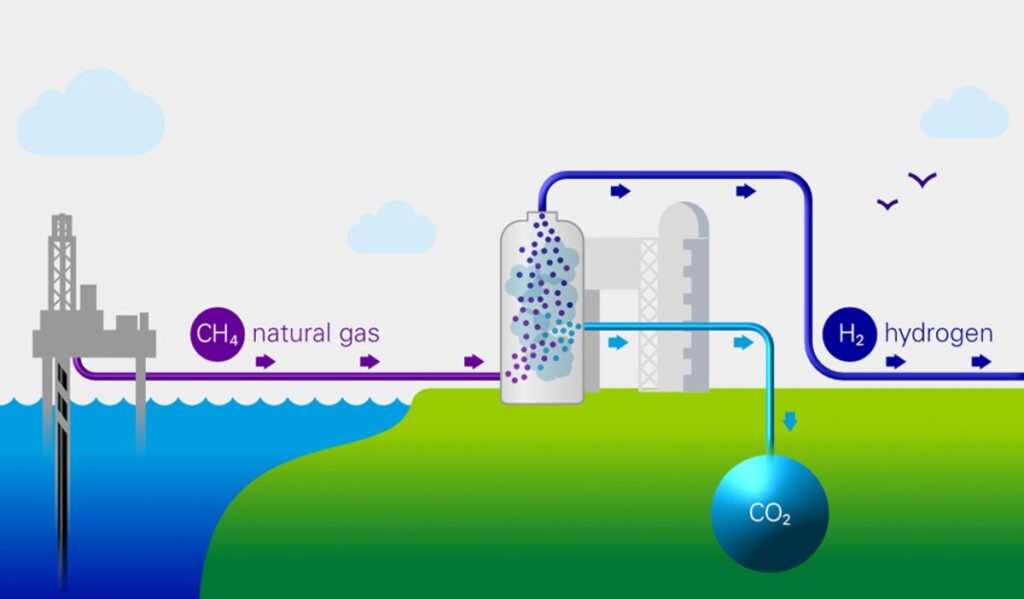

The production of blue hydrogen is primarily categorized by the technology used to reform natural gas (methane) into hydrogen.

-

Steam Methane Reforming (SMR): Currently the dominant technology, accounting for over 60% of the market share. It is a mature process where high-temperature steam reacts with methane. While cost-effective and supported by existing infrastructure, SMR produces a more diluted $\text{CO}_2$ stream, making carbon capture slightly more complex and less efficient than newer methods.

-

Autothermal Reforming (ATR): This is the fastest-growing technology segment. ATR uses oxygen and carbon dioxide or steam to react with methane. The primary advantage of ATR is that it produces a concentrated, high-pressure 7$\text{CO}_2$ stream, allowing for carbon capture rates exceeding 98-99%. Major upcoming projects, such as ExxonMobil’s Baytown facility, are opting for ATR to maximize environmental compliance and efficiency.

Gas Partial Oxidation (POX): A smaller but significant segment, often used when processing heavier feedstocks or in specific industrial clusters where pure oxygen is readily available.

Key Application Segments

Blue hydrogen is not a “one-size-fits-all” solution; its adoption varies significantly across different industrial verticals.

1. Petroleum Refineries

The refining sector is currently the largest consumer of blue hydrogen. Refineries use hydrogen to desulfurize fuels and crack heavy hydrocarbons. By switching from “gray” hydrogen (unabated natural gas) to blue, refineries can drastically reduce their scope 1 emissions without overhauling their entire core infrastructure.

2. Chemical Industry (Ammonia & Methanol)

Ammonia production is a cornerstone of global food security (fertilizers). The transition to “Blue Ammonia”—ammonia made using blue hydrogen—is gaining massive momentum. In 2025, major investments by companies like Linde and OCI Global in the US Gulf Coast have solidified this segment as the fastest-growing application for low-carbon hydrogen.

3. Power Generation

Blue hydrogen is increasingly viewed as a dispatchable, carbon-neutral fuel for power plants. By blending hydrogen into natural gas turbines or using 100% hydrogen-ready turbines, utilities can provide “firm” carbon-free power to complement the intermittency of wind and solar.

4. Heavy-Duty Transportation

While battery-electric vehicles dominate the passenger car market, fuel-cell electric vehicles (FCEVs) powered by blue hydrogen are targeting the heavy-duty sector. Long-haul trucks, marine vessels, and even trains are utilizing blue hydrogen due to its high energy density and fast refueling times compared to batteries.

Regional Analysis: The Rise of Hydrogen Hubs

The geography of the blue hydrogen market is defined by two factors: access to cheap natural gas and proximity to geological $\text{CO}_2$ storage sites.

-

North America: The clear leader, holding over 40% of the market share. The US Gulf Coast (Texas and Louisiana) has become the global epicenter for blue hydrogen, fueled by the Inflation Reduction Act (IRA). Tax credits like 45Q (for carbon sequestration) and 45V (for clean hydrogen production) have made blue hydrogen projects in the US some of the most bankable in the world.

-

Europe: Focused heavily on the North Sea region. Countries like the UK, Norway, and the Netherlands are leveraging depleted offshore gas fields for $\text{CO}_2$ storage. The European Green Deal and high carbon prices (EU ETS) make blue hydrogen a vital tool for the continent’s industrial heartlands.

-

Asia-Pacific: Driven by energy-importing giants like Japan and South Korea. These nations are establishing “blue ammonia” supply chains with exporters like Australia and Saudi Arabia to decarbonize their power sectors.

-

Middle East: Players like Saudi Aramco and ADNOC are investing billions to leverage their low-cost gas reserves, aiming to become the world’s leading exporters of blue hydrogen and its derivatives.

Market Drivers and Trends

-

Policy Support: The finalization of clean energy tax rules in 2025 has provided the “regulatory certainty” that investors long craved. Policies like the US 45V credit provide up to $3 per kg of clean hydrogen, drastically improving the internal rate of return (IRR) for large-scale facilities.

-

Carbon Pricing: As carbon taxes rise globally, the cost penalty for “gray” hydrogen increases, making the premium for blue hydrogen more palatable for industrial offtakers.

-

Infrastructure Synergies: The ability to repurpose existing natural gas pipelines for hydrogen blending allows for a faster rollout than green hydrogen, which often requires entirely new, dedicated infrastructure.

Challenges and Market Restraints

Despite the bullish outlook, the blue hydrogen market faces critical scrutiny:

-

“Methane Leakage”: The environmental credibility of blue hydrogen depends entirely on minimizing methane leaks during gas extraction. High leakage rates can negate the climate benefits of carbon capture.

-

Competition from Green Hydrogen: As the cost of electrolyzers and renewable energy continues to fall, green hydrogen (made from water and renewables) will eventually achieve price parity with blue, potentially limiting the “bridge” period for blue assets.

-

Public Perception: Some environmental advocates view blue hydrogen as a way to prolong the life of the fossil fuel industry, leading to stricter “additionality” and “purity” requirements in some jurisdictions.

Competitive Landscape

The market is dominated by global industrial gas giants and “Big Oil” firms pivoting toward energy services.

-

Linde PLC: A leader in integrated hydrogen solutions, from production to distribution.

-

Air Liquide: Heavily involved in European hydrogen clusters and high-tech carbon capture membranes.

-

Air Products and Chemicals: Known for massive world-scale projects, including the $4.5 billion blue hydrogen complex in Louisiana.

-

ExxonMobil & Shell: These companies are leveraging their sub-surface expertise to dominate the $\text{CO}_2$ storage aspect of the blue hydrogen value chain.

Future Outlook

The next five years (2025–2030) will be the “era of the FID.” Projects that break ground today will define the global energy landscape of the 2030s. While green hydrogen remains the ultimate goal for a fully circular economy, blue hydrogen is the essential workhorse that allows heavy industry to begin its decarbonization journey today.

By leveraging existing gas assets and scaling carbon capture technology, the blue hydrogen market is proving that the path to net-zero is not just about building the new, but also about intelligently transforming the old.

Other Report Zion Market Research:

www.zionmarketresearch.com/de/report/magnesium-alloys-market

www.zionmarketresearch.com/de/report/collimating-lens-market

www.zionmarketresearch.com/de/report/online-on-demand-laundry-service-market

www.zionmarketresearch.com/de/report/hypercharger-market

www.zionmarketresearch.com/de/report/plant-based-protein-market